Frederick Peters

President Emeritus

Climbing interest rates, falling stock prices, contested elections with new ones upcoming? Recession talk abounds as the summer of 2022 moves into fall. While the job market remains strong, the prevailing mood in New York City is one of disquiet. The real estate market, often a trailing indicator, has been gradually adjusting over the third quarter; many sales prices are down (though not all) and the spike in inventory which would have given buyers more options has failed to materialize at hoped-for levels. The city has entered what I like to call a “tornado market:” one property receives multiple offers while the similar one next door sits idle with nary a showing request. While much of this may be attributable to condition (supply chain issues and co-op Boards still make many buyers wary of apartments needing renovation), there remains a quality of randomness to what sells and what doesn’t. That said, throughout the quarter, prices continued to differentiate based on size, property type, and location.

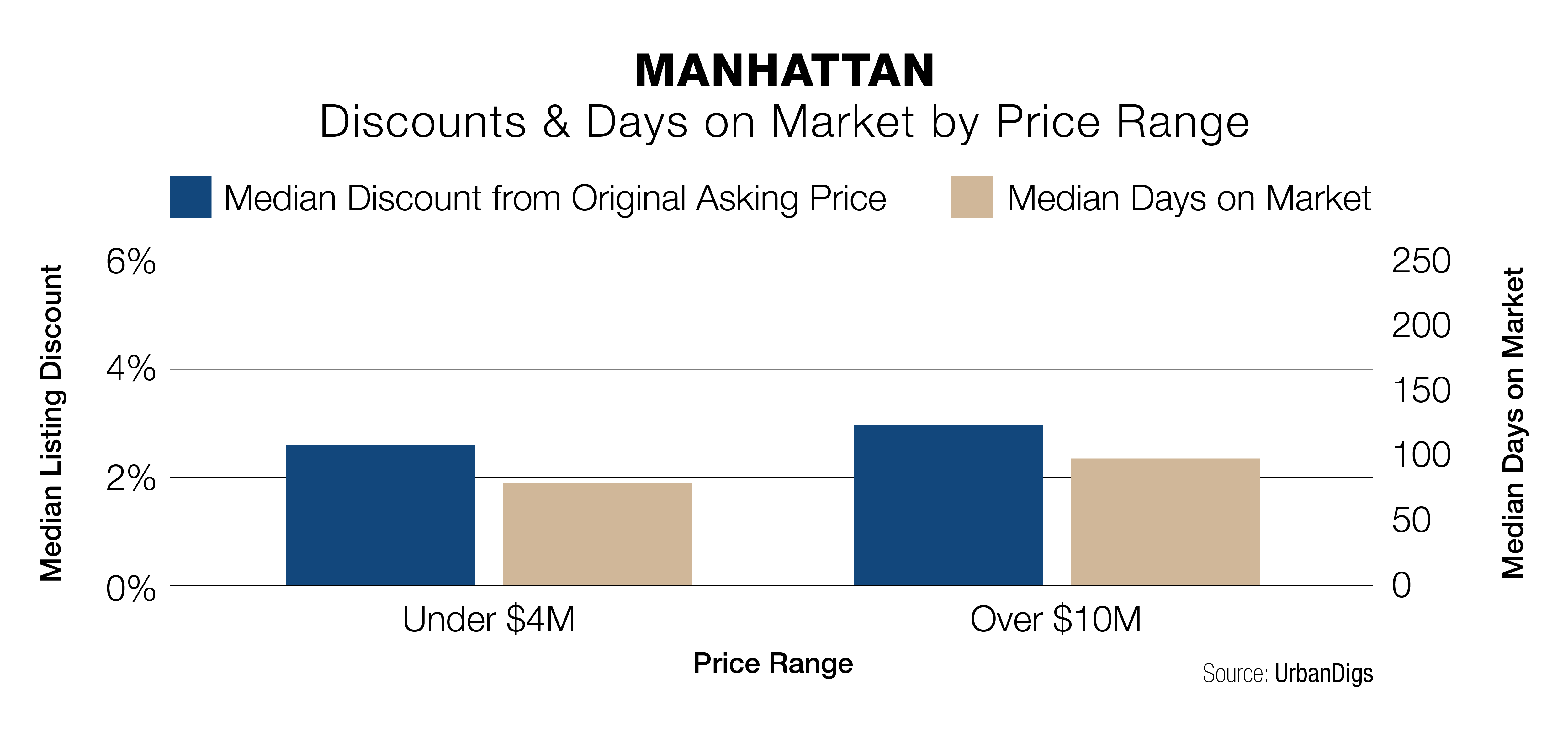

Size | Smaller and midsized properties traded far more briskly throughout the third quarter than larger units. For much of the summer, the greatest condo sales activity occurred in Brooklyn and Queens; in Manhattan sales were the most brisk for smaller units. While there were sales of marquee properties, in general the $10 million and above condo market was considerably quieter than at this time last year. Townhouse sales reflected a similar bias: with few exceptions, the properties above $10 million are lingering on the market. And in the co-op market many of the beautiful large pre-war apartments along Park and Fifth Avenues and Central Park West which have been aspirational homes for so many New Yorkers now linger for months, even years, without buyers.

Property Type | As a general rule, the simpler ownership experience offered by condominiums continues to appeal to buyers. With their beautiful amenity floors offering everything from meeting rooms to movie theaters, from restaurants to professional level fitness centers, these luxurious newly built buildings offer the ease of a move-in ready home. In the pandemic world, fewer buyers than ever have the inclination to embark on a soup-to-nuts renovation. As noted above, supply chain issues, and the vagaries of co-op Boards which must approve renovations, further incline prospective buyers away from older units in need of upgrading. As more and more condominiums rise in all parts of the city, more and more New Yorkers, both those new to the city and those who have been here forever, choose this form of ownership. While many co-op dwellers now move to condos, the converse is rarely if ever true.

Location | Nice two bedroom, two bath units on the Upper West Side, even those needing work in older co-ops, sold throughout the summer within a few weeks. Meanwhile, their counterparts on the Upper East Side seemed to spend more time on the market and then sell for less. Everything in the Village, if it is priced right and not too quirky, sells briskly, including properties in the East Village where no one who had a choice would have considered living forty years ago. Meanwhile, many Harlem properties move slowly and, among the newer condominiums, at prices lower than those which the current owners paid for them. Brooklyn remains hot but nonetheless slower than it was a year ago; the Brooklyn frenzy has abated.

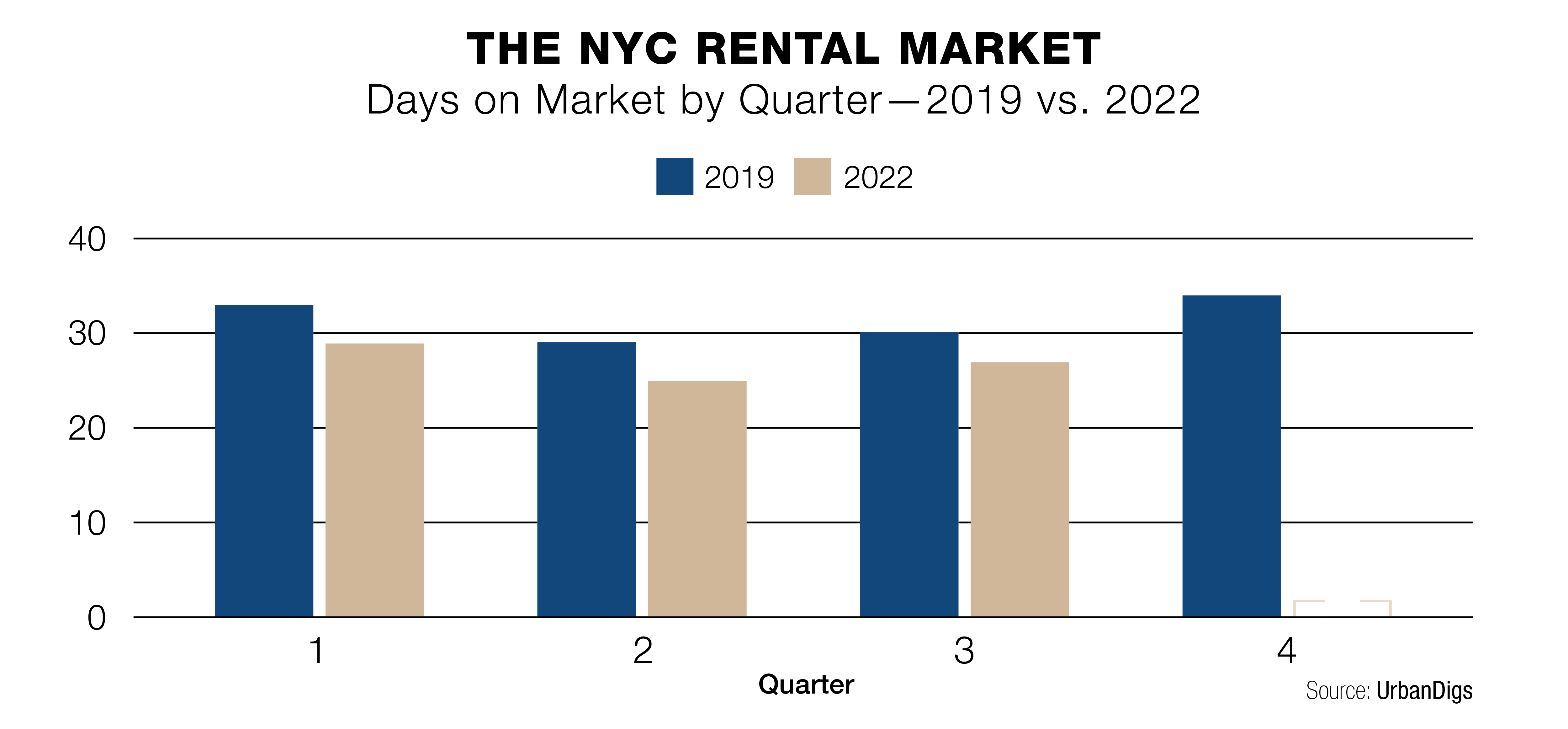

During the third quarter, the NYC rental market continued to experience the unprecedented run up in prices which began earlier in the year. Inventory has been thin, and during much of the summer prospective tenants were offering in excess of the asking rent just to secure the property. While the market has cooled a little in September, this remains one of the tightest quarters in recent history for inventory in the rental market.

And what can we expect in the coming months? As the Fed continues to push rates up in order to combat inflation, and these rate increases continue to have a negative impact on stock prices, a mild recession seems increasingly likely even as unemployment remains low. Prices will thus continue a mild contraction throughout the fourth quarter, especially in the lead up to the midterm elections.

Buyer opportunities will abound for those brave enough to look past the current economic trends to the longer term value in real estate ownership.