Frederick Peters

President Emeritus

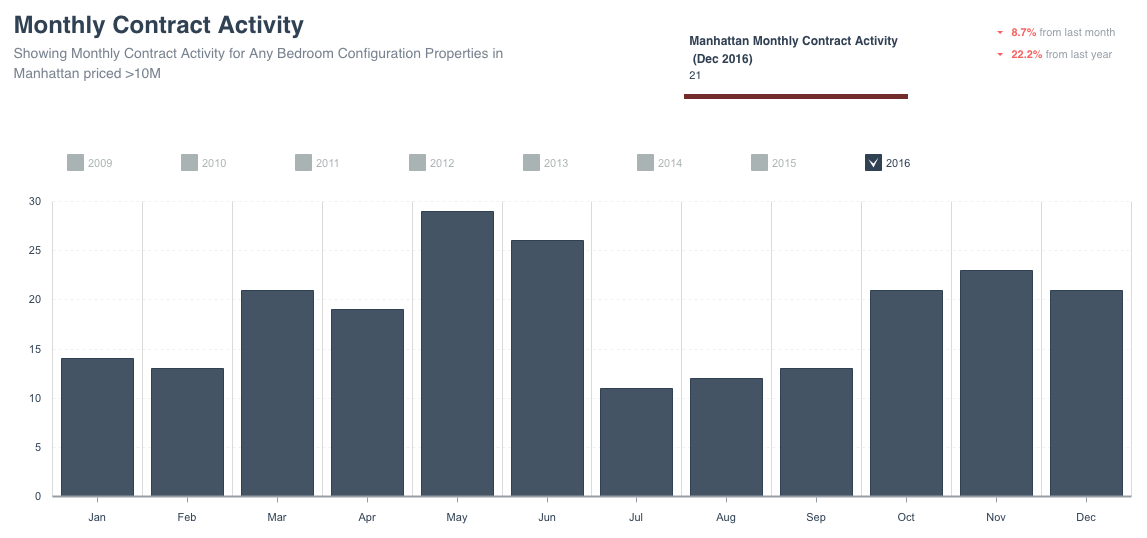

Like the Presidential elections, the 2016 New York real estate market ended with a bang. Within a week of November 8, the market, which had been idling since July, kicked into gear. The early weeks of December saw more transactions over $4 million than any time since the spring, and other sectors benefited as well. The last six weeks of 2016 saw a level of transactional activity which ordinarily accompanies a looming tax change. But no tax change loomed. Instead, anticipation of a business-friendly administration on Capitol Hill, combined with relief that the whole wrenching election process was finally over, generated a dynamic response to well-priced listings, even those which had been languishing on the market for months.

The turn was most dramatic in the upper market. While there still exists an oversupply of ultra-high-end condominiums, buildings like 432 Park have experienced renewed market activity as they move into their final selling phase. In the oversupplied areas, like the greater 57th Street corridor and river to river below Canal Street, this renewal has been spurred by substantial discounting, both in the form of developer-paid closing costs (usually a buyer’s responsibility) and prices agreed at 5 to 10% below the ask. The co-op market will recover more gradually; many of the luxury co-op units are still overpriced and in relatively poor repair. The prospect of facing both the Board approval process and a renovation sends increasing numbers of buyers, both local and foreign, fleeing to the condo market, where they can acquire spacious, toothbrush-ready homes with every modern amenity.

The more moderately priced condominiums being built in the 80s and 90s on the Upper East and West Sides fared extremely well during the latter half of 2016 (of course, “moderately priced” is a relative term, as these units tend to cost between $1.5 million and $8 million.) These units, constructed in established residential neighborhoods and offering modern conveniences close to schools and parks, entice families and other buyers looking for spacious new quarters; the opening on January 1 of the Second Avenue Q line subway will only add value to these new residences east of Third Avenue. For this constituency co-ops increasingly attract by relative value; when the discount compared to a new building is substantial enough, the hassle of Board approval and upgrading become tolerable.

Source: UrbanDigs

Smaller apartments drove real estate markets in every borough throughout the year. One- and two-bedroom apartments, priced under $2 million, outperformed every other sector both in volume and in relative sales prices. These smaller homes experienced enormous demand with which supply could not keep up. Even during the early fall, when demand for most offerings slowed to a trickle, buyers were still competing for 3-, 3.5-, and 4-room apartments – with the caveat that they were sensibly priced. 2016 simply was not a year during which buyers overpaid in any price range. And they had all done their homework, so they knew the comparable sales and did not display much flexibility about their price limits. Somewhere around July, this turned into a buyer’s market.

Usually the rental market surges when sales are weak. Not so this year. Even last spring, luxury rentals were signing leases at 10, 15, even 20% below what they had achieved two years earlier. While overpricing hobbled some segments of the rental market, even those units at the lower end which usually enjoy quick turnaround have been slow. Since the winter market for rentals is historically in the doldrums, we will have to wait for spring to get a sense of how strongly, and at what prices, this market will bounce back.

While the Brooklyn market experienced the same ebbs and flows as those described above, the ongoing demand/supply imbalance protected prices in most neighborhoods. Competitive bidding remained common throughout the year, and prices in Brooklyn today have risen enough so that many buyers are turning back to Manhattan because neighborhoods such as the far East Side, Upper Harlem, and Washington Heights offer them better value.

Overall, the two most significant real estate markers of the past year pertain to co-op values and shifting market dynamics. 2016 made evident in no uncertain terms the ongoing challenges implicit in co-op ownership: Board expectations and demands on the one hand and condition on the other. With a number of perfectly qualified candidates rejected by Boards who believed the sales prices were too low, agents and sellers alike are placed in a quandary. No one WANTS to accept a low price; the deal that gets made is always the best deal available at the time. For Boards to then reject the opinion of the market diminishes the quality of the co-op asset and drives more buyers towards the relative ease of condominium purchases. For buyers to jump through the hoops required for co-op approval, only to learn that the Board feels they are not paying enough, frequently drives a decision to cross co-ops off the list. Furthermore, almost every co-op needs SOME renovation. Little wonder that for many buyers, value versus condominiums becomes one primary motivation to consider a co-op purchase, the other being location. A buyer whose heart is set on a pre-war palace on Fifth Avenue or Central Park West remains, like it or not, a co-op buyer.

2016’s other most significant development was the shift from seller’s market to buyer’s market. Increasingly, as the year went by, buyers possessed the upper hand; they balked at overpricing and waited sellers out. On the listing side, 2016 was a year of price drops, often multiple, to position the subject properties for sale in the changed marketplace. While the year began with sellers firmly in charge of the market, December saw almost every sale negotiated, often from prices which had already been reduced several times.

As to 2017, we face the wild card of the Trump Presidency. While I anticipate our market, like securities, will remain strong for the sale of properly priced property, predicting out beyond four to six months seems specious. Given how little we know about how well Trump and the Congress will work together, and what their disparate priorities may be, we will just have to wait and see.