Frederick Peters

President Emeritus

During the 4th quarter of 2023, several of the trends that have held the residential real estate market back for much of the year have begun to ease. Inflation seems to be cooling. The Fed did not raise the prime rate at its last meeting, and mortgage rates have begun a gradual descent. Most importantly, many sellers who clung throughout the earlier part of the year to stubbornly high prices for their properties have concluded that they must compromise if they wish to sell. This marketplace is not kind to mispriced property.

The first three quarters of 2023 presented significant challenges to both buyers and sellers. Interest rates, already high as 2022 ended, continued to escalate throughout much of the year. Concern about the ongoing war in Ukraine became exacerbated on October 7th, as the 4th quarter began, when the Hamas attack on Israel precipitated another regional conflict into which the United States was drawn.

The purchase of residential real estate represents both a belief and an investment in the future. As the city continues to emerge, almost four years later, from the disruption created by COVID, certain signs of urban health have asserted themselves. Restaurants remain busy, as do concert halls and theaters. Tourists once again cause pedlock on the Midtown avenues. And there is a little more inventory for sale throughout the marketplace.

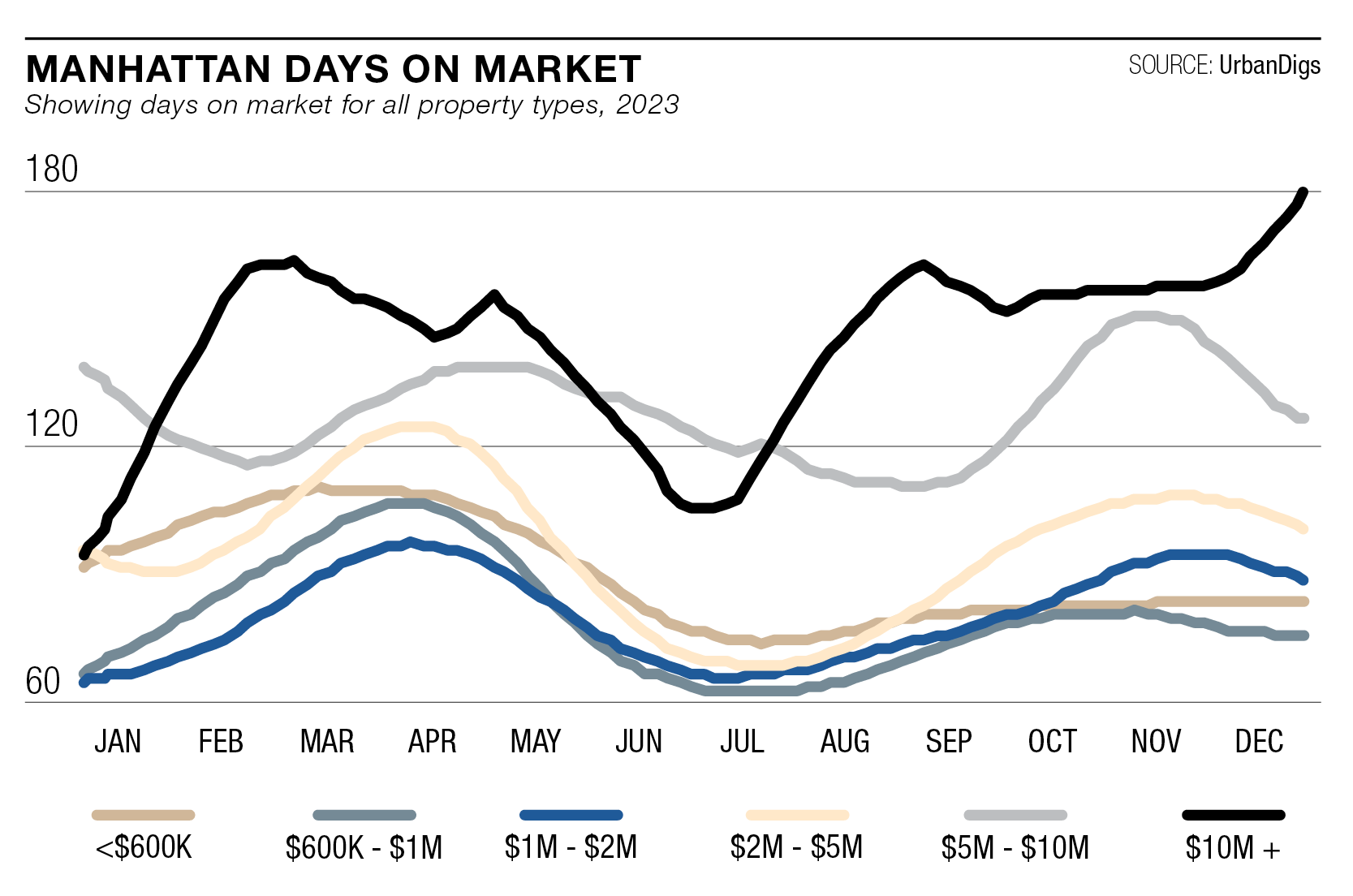

Still, the sales markets in New York City have not experienced a robust year. Big ticket items in particular moved slowly, especially in the increasingly challenged co-op marketplace. Many of New York’s luxury co-ops, especially those priced in excess of $10 million, have “celebrated” market anniversaries and moved into their second year of availability. The trade of smaller units has been brisker, but even in the one and two-bedroom markets, many properties have remained available for months. One interesting sidebar: ordinarily a tight and expensive rental market (which we have experienced in 2023, even though demand has slowed somewhat from the rental frenzy of 2022) drives sales prices up as more people decide that they would prefer to own rather than pay what they deem exorbitant rental costs. But that’s not the case this year. The tight rental market, in all price ranges and boroughs, has frustrated prospects but doesn’t seem to have driven them into the purchase market, probably on account of relatively high interest rates. That same issue also accounts for the ongoing (although somewhat improved) dearth of inventory nationwide. Many buyers must sell their own properties first. And many of those don’t wish to sacrifice a mortgage at 2.8% to go into a new one at 6.8%. Renovations are booming nationwide as many buyers decide to remain in their current home and upgrade it rather than buy a new home and pay $6.80 in interest for every hundred dollars borrowed rather than the $2.80 that they are paying now.

On a more micro level, trends that began earlier in the century become more codified every year:

TRIBECA RISING 10013, the zip code for Tribeca, remains the priciest in New York City, driven primarily by its inventory of ultra-high-end condominiums. The Upper East Side, once the city’s bastion of wealth and privilege, offers mostly co-ops, which, as noted above, appeal less to today’s younger wealthy entrepreneurs both because of the onerousness of co-op approval process and the fact that most co-op apartments need renovation, which in today’s world can add millions to the price and years to the timeframe.

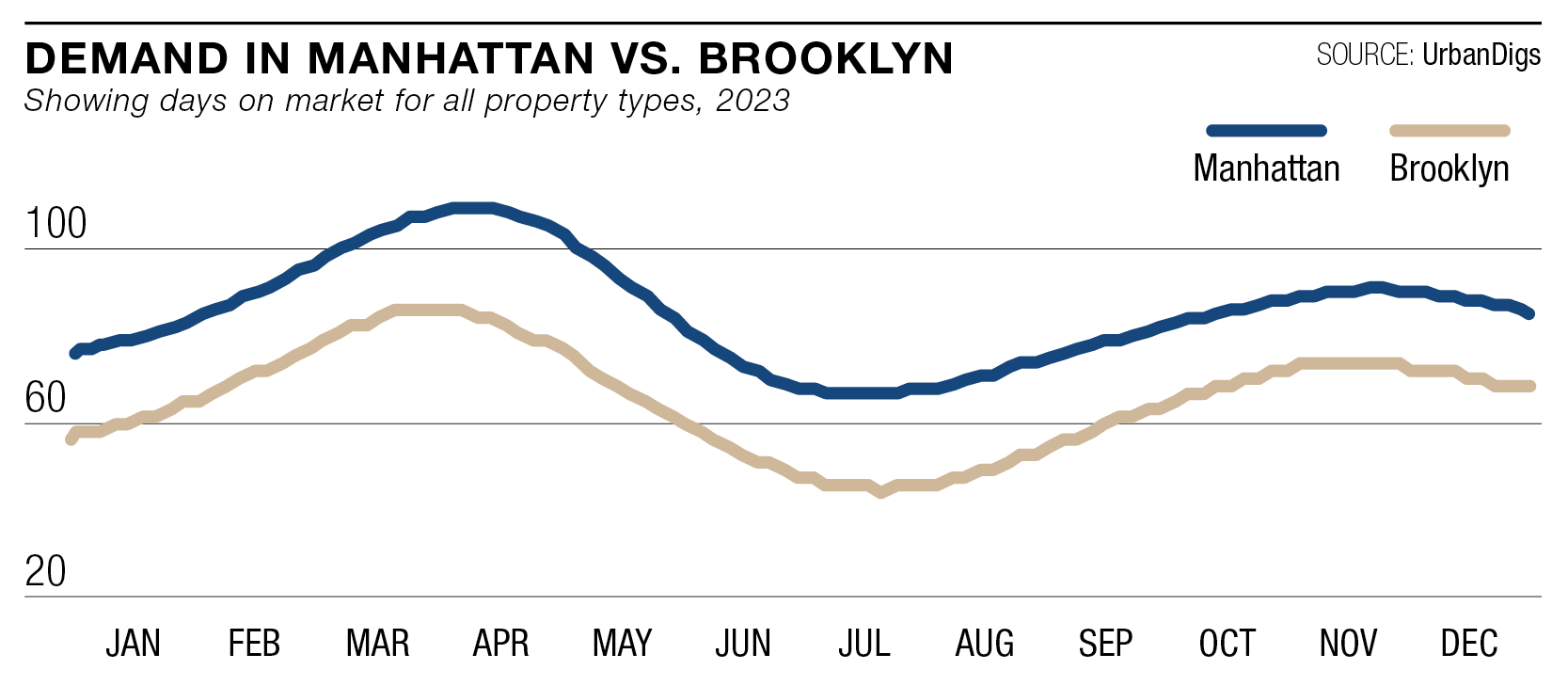

HOT SPOTS Brooklyn, especially north Brooklyn, remains a particular market hotspot, with prices remaining higher (relative to market-peak 2016 numbers) and days on market lower than in Manhattan.

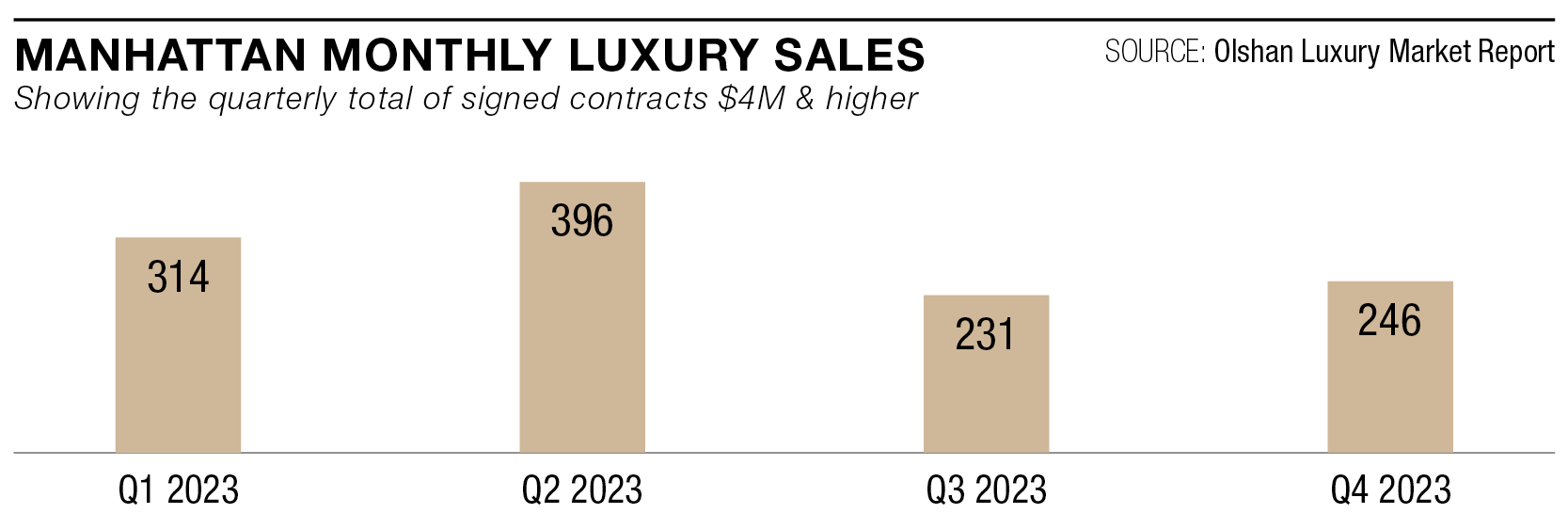

$4 MILLION+ SALES INCREASE Manhattan sales of homes at $4 million and over crept up again in the latter half of the 4th quarter, according to the Olshan Report. These larger deals slumped during August, September, and October: the average number of sales per week between August 7 and October 30th was 16, while between November 1st and December 18th (counting Thanksgiving as a half week), it hit 21.

Looking forward into 2024, we project that the easing of mortgage costs will continue, although they will not sink close to the rates many consumers became accustomed to during the decade that ended in 2021. Hopefully, there will be an increase in properly priced inventory as serious sellers continue to recognize that optimistic pricing yields no results. The wars in Ukraine and the Middle East seem poised to continue into much of 2024, even as the bitterly contested Presidential election draws closer. Do not look to 2024 as a year of buoyant price increases. But there will continue to be pockets of real opportunity, most particularly in co-ops or more peripheral neighborhoods, for buyers ready to make a purchasing decision.

Originally published on Forbes